Scope 3 Emissions: Your Guide To Get Started

- 5 mins

- Gemma Branney

For most companies, over 70% of their climate impact lies outside their own operations. This is Scope 3: the hardest, most consequential, and most misunderstood part of corporate carbon accounting.

What is Scope 3 reporting?

Scope 3 reporting is the process of measuring and disclosing the indirect greenhouse gas (GHG) emissions that occur across a company’s entire value chain from the extraction of raw materials by its suppliers to the eventual disposal of its products by end users.

The three scopes of corporate emissions are defined by the GHG Protocol Corporate Standard. Scope 1 is emissions directly from sources you own and control including fuels, gas and vehicles. Whereas Scope 2 is purchased electricity, heat and steam, and EV. And Scope 3 is indirect emissions from supply-chains to investments.

The GHG Protocol’s Corporate Value Chain (Scope 3) Accounting and Reporting Standard, provides the definitive methodology for measuring these emissions. Unlike Scopes 1 and 2, which are largely within a company’s operational control, Scope 3 requires collaboration with and data from hundreds or thousands of external parties.

Why it matters

A 2023 analysis by CDP (formerly the Carbon Disclosure Project) found that Scope 3 emissions represent, on average, 11.4 times the operational (Scope 1 + 2) emissions of the companies that report them. For sectors like financial services, retail, and technology, this ratio is often 50:1 or higher.

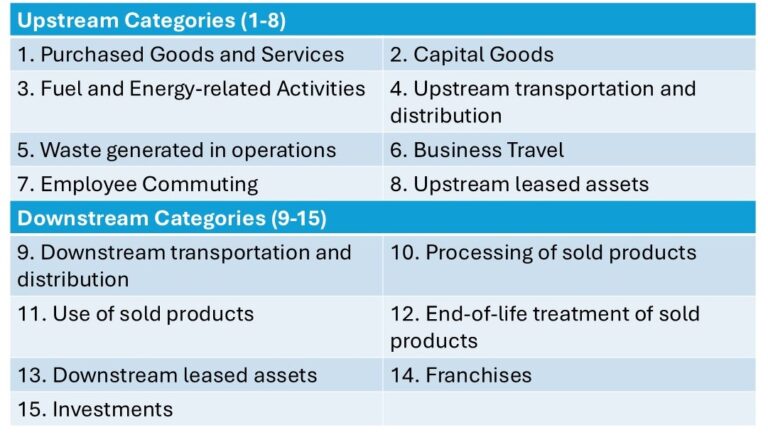

The 15 categories of Scope 3 emissions

The GHG Protocol divides Scope 3 into 15 distinct categories: 8 upstream (related to a company’s supply chain) and 7 downstream (related to how products are used and disposed of after sale). Each category has specific accounting boundaries, activity data requirements, and emission factor sources.

How to measure Scope 3 emissions

There are three primary calculation approaches for Scope 3 emissions. In practice, most organisations use a combination depending on the category and data availability.

Spend-based: Expenditure multiplied by economically input-output emission factors (EIO). The most common approach, based on a model rather than activity specific. It does mean if you have sustainability policies in place the carbon reduction won’t be applied.

Supplier specific: Emissions factors derived directly from individual supplier product-level data. This means collecting data directly from your suppliers and means any sustainable procurement decisions made will be reported.

Hybrid: Using both supplier specific and spend-based e.g. collecting data for your top tier suppliers only due to resource, and likely your larger suppliers will be reporting emissions already which makes sourcing data easier.

Simple Step-By-Step Guide

Most organisations approaching Scope 3 for the first time should phase their effort rather than attempting comprehensive primary data collection immediately. The following sequence is a helpful way to plan your reporting:

Screen all 15 categories. Use budgets or sector average methods to produce order-of-magnitude estimates across all categories. This step takes weeks, not months, and is essential for directing resources to where they matter.

Identify your material categories. In most organisations, 2 – 4 categories account for over 90% of Scope 3 footprint. For a bank, this will almost certainly be Category 15. Whereas a tech company, it may be Categories 1, 6, and 7. Confirm this before investing in complex data collection so you invest time in the most impactful areas.

Improve data quality in material categories. Engage directly with the relevant counterparties (suppliers, borrowers, investees, or your own employees to) gather primary data. For Category 15, this means engaging portfolio companies. For Category 6, it means integrating with travel management systems.

Apply hybrid methodology for the remainder. Use the best available secondary data for categories outside the material core. In the UK DEFRA is the best source of emission factors which you can find on the Government website. Document all methodological choices and data sources to ensure you are consistent year-on-year.

Set a base year and plan for improvement. Year-one inventories are almost always imprecise. The goal is to establish a defensible baseline that can be refined over successive reporting cycles, not to achieve perfection immediately. Year 2 or 3 are what we would recommend for your baseline rather than Year 1.

Common methodological pitfalls across all sectors

In our experience, several systematic errors recur in Scope 3 inventories, regardless of sector, often leading to material misstatement or challenges during third-party verification:

Confusing materiality with convenience. Many organisations report only the categories they find easy to measure which is typically business travel and waste. We often see clients under-report or omit their most material categories like supply-chain or product use due to limited resources. This produces a technically compliant but misleading inventory. Regulators and assurance providers are increasingly alert to this pattern and want to understand what categories are excluded and why.

Inconsistent organisational boundaries. Scope 3 must follow the same organisational boundary as Scope 1 and 2 (see our how to measure emissions blog).

Double-counting between categories. The GHG Protocol’s boundaries are designed to minimise double-counting, but errors occur most frequently between purchased goods and services, and other categories such as business travel or energy. Taking time to allocate data and remove duplications is important. We had a client where 30% of their carbon footprint was duplication errors.

Treating the inventory as a compliance exercise. Organisations that approach Scope 3 purely as a reporting obligation tend to produce disclosures that satisfy the letter of frameworks but offer no strategic insight. The most valuable use of a Scope 3 inventory is to identify where you have third party risks and what interventions can achieve the largest emission reductions per unit of effort. This leads to efficiencies and optimisation across your operations but also helps mitigate risks. With one client we identified significant opportunities to consolidate spending across their global operations during carbon reporting, with savings in excess of £200,000.

Disclosure frameworks and regulation

Scope 3 disclosure has moved from voluntary best practice to mandatory requirement in several major jurisdictions. Understanding which frameworks apply to your organisation is essential for compliance planning.

EU Corporate Sustainability Reporting Directive (CSRD)

Mandatory · EU · Phased from 2025

Requires disclosure under the European Sustainability Reporting Standards (ESRS). ESRS E1 mandates Scope 3 reporting for large companies (1000+ employees and €450m in annual turnover). The most comprehensive mandatory regime globally.

Taskforce for Climate-related Financial Disclosures Recommendations

Mandatory · UK

TCFD is a reporting requirement for premium listed companies and Large UK-registered companies and LLPs with 500+ employees and £500m+ turnover. The framework is across governance, strategy, risk management and metrics/targets. This often includes Scope 3 due to materiality.

USA Climate Disclosure Rules

Mandatory · State Regulation

The SEC’s 2024 rule is currently on hold and likely will remain that way until 2029. California’s SB 253 requires businesses with annual revenues over $1 billion that do business in California to disclose Scope 1 and 2 emissions starting in 2026, and Scope 3 emissions starting in 2027. Illinois and Colorado have introduced similar legislation.

ISSB IFRS S2 Climate Standard

Voluntary baseline · Global

The ISSB’s S2 standard requires Scope 3 disclosure where material, using GHG Protocol methodology. Increasingly adopted as a baseline by national regulators including the UK, Australia, and Canada.

CDP Climate Change Questionnaire

Voluntary · Global · Investor-driven

CDP requests complete Scope 3 disclosure across all 15 categories. CDP scores are used by institutional investors and procurement teams; non-disclosure is often scored as a reputational risk.

Science Based Targets initiative (SBTi)

Voluntary target-setting · Global

SBTi requires companies to set Scope 3 reduction targets if Scope 3 exceeds 40% of total footprint. The SBTi Corporate Net-Zero Standard requires net-zero targets across all scopes by no later than 2050. This is a best practice framework. Most clients and lenders expect SBTi aligned targets, set using the target setting tools.

Frequently asked questions

Is Scope 3 reporting mandatory?

It depends on your jurisdiction and company size. Under the EU CSRD, Scope 3 is mandatory for very large companies. The UK is developing its own Sustainability Disclosure Standards (UK SDS) aligned to ISSB S2, which will require Scope 3 where material. The USA it varies from State to State. Investor pressure through CDP and institutional engagement frameworks often require Scope 3 reporting.

What is the difference between the GHG Protocol and ESRS?

The GHG Protocol Corporate Value Chain Standard is the underlying accounting methodology. It defines what counts as Scope 3, how to set boundaries, and how to calculate emissions. ESRS E1 is a disclosure standard that specifies what information companies must report and how they must present it. It explicitly references and requires compliance with the GHG Protocol methodology. In other words, GHG Protocol is the measurement standard; ESRS is the reporting standard built on top of it.

How do I know which Scope 3 categories are relevant for my company?

A category is “relevant” if it is large in magnitude relative to total emissions, if it offers significant reduction potential, or if key stakeholders (investors, customers, regulators) consider it important. Start with a screening assessment using your budget and placing spend values across all 15 categories to identify which are material. For most companies, only 3–6 categories will account for over 90% of Scope 3 emissions. The GHG Protocol provides specific relevance criteria in Appendix B of the Corporate Value Chain Standard.

Can I exclude categories from my Scope 3 inventory?

Yes, but only if you can demonstrate that the excluded categories are not relevant using the GHG Protocol’s relevance criteria. You cannot exclude categories simply because they are difficult to measure. Under CSRD and ESRS E1, any exclusion must be explicitly disclosed and justified. Categories that are excluded due to lack of data rather than genuine immateriality are likely to be flagged by assurance providers.

What is a Scope 3 base year, and when do I need to recalculate it?

A base year is a historical reference point against which progress is measured. The GHG Protocol requires companies to establish a base year and recalculate it when “significant structural changes” occur, such as mergers, acquisitions, divestitures, or material changes in methodology. Minor year-on-year variations in measurement approach do not require recalculation. The SBTi requires a base year no earlier than 2015 for targets submitted under the Net-Zero Standard.

Need Support?

ENVOLV partners with clients to design robust carbon reporting methodologies across Scope 1, 2 and 3. From fast paced advice to full, compliant carbon reporting and net zero transition planning, we deliver expertise that move you forward.

For a free consultation and review of your current reporting approach get in touch.