SECR Reporting: The Complete UK Guide

- 4mins

- Gemma Branney

Quick answer: Streamlined Energy and Carbon Reporting (SECR) is a mandatory UK regulation requiring large companies and LLPs to disclose their annual energy use and greenhouse gas emissions in their Directors’ Report. If you meet two of three qualifying thresholds: £36m+ turnover, £18m+ balance sheet, or 250+ employees, then this guide is for you.

What is SECR reporting?

Streamlined Energy and Carbon Reporting (SECR) is a UK government framework that requires qualifying organisations to publicly disclose their energy consumption and associated greenhouse gas (GHG) emissions each year. It was introduced under the Companies (Directors’ Report) and Limited Liability Partnerships (Energy and Carbon Report) Regulations 2018.

The framework is designed to increase corporate transparency, encourage energy efficiency action, and provide investors and stakeholders with clear, comparable data on a company’s environmental impact.

Who needs to comply?

Three categories of organisation are in scope for SECR reporting:

- Quoted companies — any UK-incorporated company listed on a regulated stock exchange, regardless of size.

- Large unquoted companies — private UK-incorporated companies meeting at least two of the three size thresholds below.

- Large LLPs — limited liability partnerships satisfying the same two-of-three criteria.

Companies who are in one of those categories and meets 2 of 3 size thresholds below must comply with SECR:

- £36m+ annual turnover

- 250+ employees

- £18m+ balance sheet

One key exemption applies: if your organisation qualifies as large but consumed fewer than 40,000 kWh (40 MWh) of energy during the reporting period, you are classified as a low energy user and are exempt from full disclosure. You must, though, include a statement to that effect in your Directors’ Report.

What must your SECR report include?

Requirements differ slightly depending on whether you are a quoted company or a large unquoted company or LLP. Here is what each must disclose:

Quoted companies

- Global Scope 1 and Scope 2 GHG emissions (tonnes CO₂e)

- Underlying global energy use (kWh) for the current year

- At least one emissions intensity ratio

- Prior year’s energy and emissions figures for comparison

- Narrative description of energy efficiency measures taken

- Methodology statement (conversion factors, standards used)

Large unquoted companies and LLPs

- UK energy use from gas, electricity, and transport fuel (kWh)

- Associated UK Scope 1 and Scope 2 GHG emissions

- At least one emissions intensity ratio

- Prior year comparative figures

- Energy efficiency actions narrative

- Methodology used

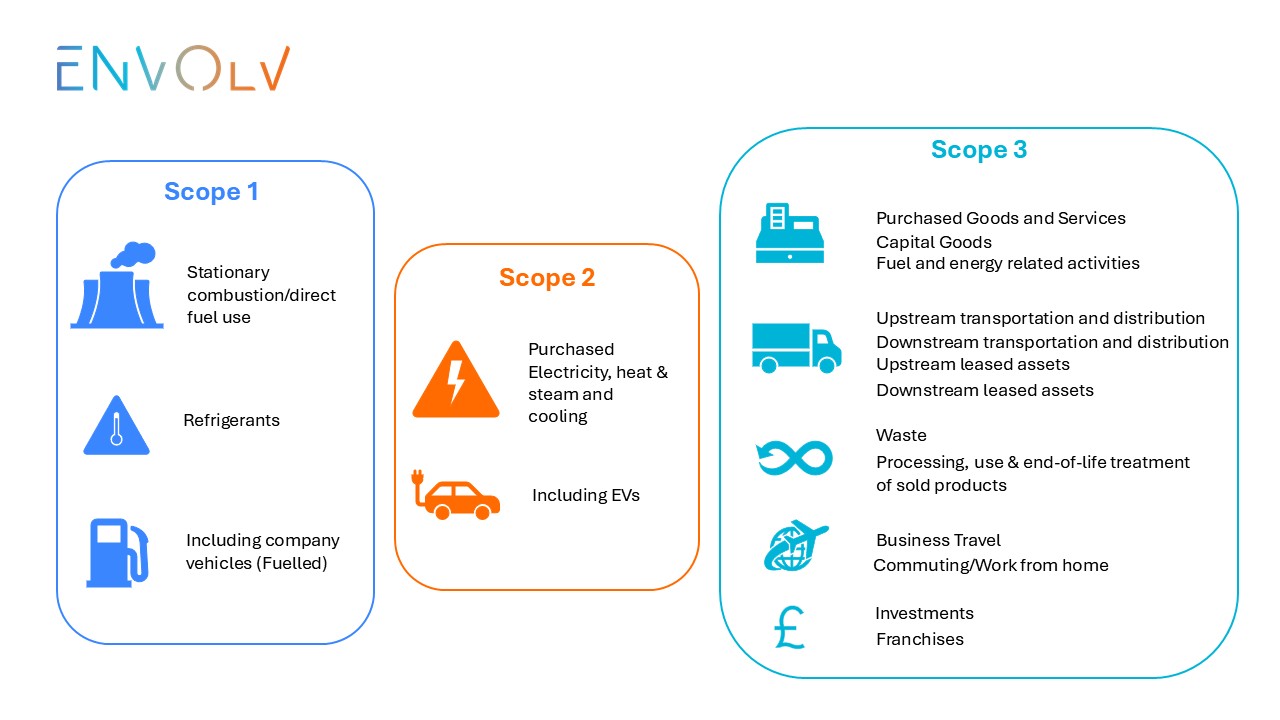

Understanding Scope 1, 2 and 3

Scope 1: direct emissions. Gas combustion on-site, company owned vehicles, industrial processes emissions.

Scope 2: in direct emissions. Purchased electricity, heat and steam, cooling, EV.

Scope 3: other indirect. Business travel, supply-chain, product.

A full carbon reporting guide across Scope 1, 2 and 3 can be found here.

Scope 3 is voluntary at the moment but we do recommend reporting or beginning to phase reporting, especially if you are setting net zero targets. We have published a complete Scope 3 guide here.

For business travel specifically, companies must include fuel purchased for rental cars or employee-owned vehicles where the organisation is responsible for that cost. Flights and train travel fall under Scope 3, which is optional but widely reported as best practice.

Emissions intensity ratios

Every SECR report must include at least one intensity ratio (a figure that normalises your emissions against a relevant business metric). This enables meaningful comparison over time and between organisations of different sizes. Common intensity metrics include:

- Tonnes of CO₂e per £million turnover

- Tonnes of CO₂e per full-time equivalent (FTE) employee

- Tonnes of CO₂e per square metre of floor space

- Tonnes of CO₂e per unit of output or production volume

Choose a ratio that makes strategic sense for your sector. Intensity on turnover can be helpful if you have business customers who would like to report your emissions as part of their supply-chain reporting.

Deadlines and submission

Financial year end: your reporting period closes. All energy and emissions data must cover this full 12-month window.

Within 9 months (plcs) / 3 months (private): Annual report and accounts, including the SECR section, must be filed at Companies House. For example, a 31 March year-end means a 30 June deadline for private companies.

Each subsequent year: prior-year comparatives become mandatory from your second reporting year onwards. Conversion factors are updated annually (typically in June), ensure you use the factors that cover the majority of your reporting year.

Penalties for non-compliance

The Financial Reporting Council (FRC) oversees SECR enforcement. Companies submitting inadequate disclosures may have accounts rejected by Companies House, triggering late-filing fines of £150 to £7,500 depending on company type and delay length. The FRC’s Conduct Committee can also impose civil penalties of up to £50,000 and issue public censures — a reputational risk that is increasingly material for ESG-focused investors.

The “comply or explain” provision

SECR contains a pragmatic comply-or-explain clause: companies may omit specific information if it is genuinely not feasible to collect, provided they clearly state what has been excluded and why. However, omitting information is strongly discouraged, and organisations should commit to providing complete data in future reporting periods. Auditors must verify that any exclusions are adequately explained.

SECR vs other UK reporting frameworks

Framework | Focus | Frequency | Mandatory? |

SECR | Energy use & GHG emissions | Annual | Yes (qualifying companies) |

ESOS | Energy savings opportunities audit | Every 4 years | Yes (large organisations) |

UK SRS (upcoming) | Full climate & sustainability | Annual | Expected to supersede SECR |

TCFD / ISSB | Climate-related financial risk | Annual | Mandatory for listed companies |

It is important to note that while SECR and ESOS both relate to energy, they serve different purposes: SECR requires annual public disclosure of consumption data, while ESOS mandates a periodic internal energy audit to identify savings opportunities. Compliance with one does not satisfy the other.

Common Mistakes

- Not including energy saving reporting, e.g. what have you implemented in the reporting period to reduce your emissions and what impact has it had so far.

- Missing critical explanations in methodology including the reporting boundary, what was in and out of scope, any assumptions or restatement of data.

- Provide context. It isn’t a requirement but adding information related to climate targets, policy and stakeholder considerations provides users with important information and can demonstrate strategy and governance.

Looking ahead: UK Sustainability Reporting Standards

SECR’s scope is expected to be superseded by the emerging UK Sustainability Reporting Standards (UK SRS), which will expand disclosure requirements from energy and carbon to the full spectrum of climate and sustainability reporting. It will shift the emphasis from retrospective compliance to forward-looking strategic integration. Early preparation is essential: organisations that embed sustainability data collection now will be significantly better positioned when UK SRS requirements come into force.

We are already helping clients get ahead of SRS reporting. Book your free consultation today.

Frequently asked questions

Does SECR apply to subsidiaries?

If reporting at group level, you may exclude energy and emissions data for subsidiaries that would not qualify for SECR individually. However, group-level thresholds are assessed on aggregate figures including all subsidiaries.

Is third-party assurance required?

There is no mandatory external assurance requirement under SECR. However, auditors must review and sign off the disclosure as part of the Directors’ Report. Many organisations voluntarily seek independent verification as investor expectations around data quality rise.

Do I need a carbon reporting platform to comply?

Not necessarily. A carbon reporting platform does add value in terms of ensuring the most relevant and up to date conversion factors are used, providing audit ready reports and improving quality assurance of data however it is not essential. Some businesses build their own report using a spreadsheet or BI tool.

Who should be involved in reporting?

We always recommend having one owner responsible for SECR but you will need various people to help collect and check the data e.g. office or site managers, finance, procurement. Your draft SECR report and carbon data should be reviewed by your Audit Committee and signed off by the Board, as part of your Annual Report and Accounts governance process.